BLOCKCHAIN

1. Background

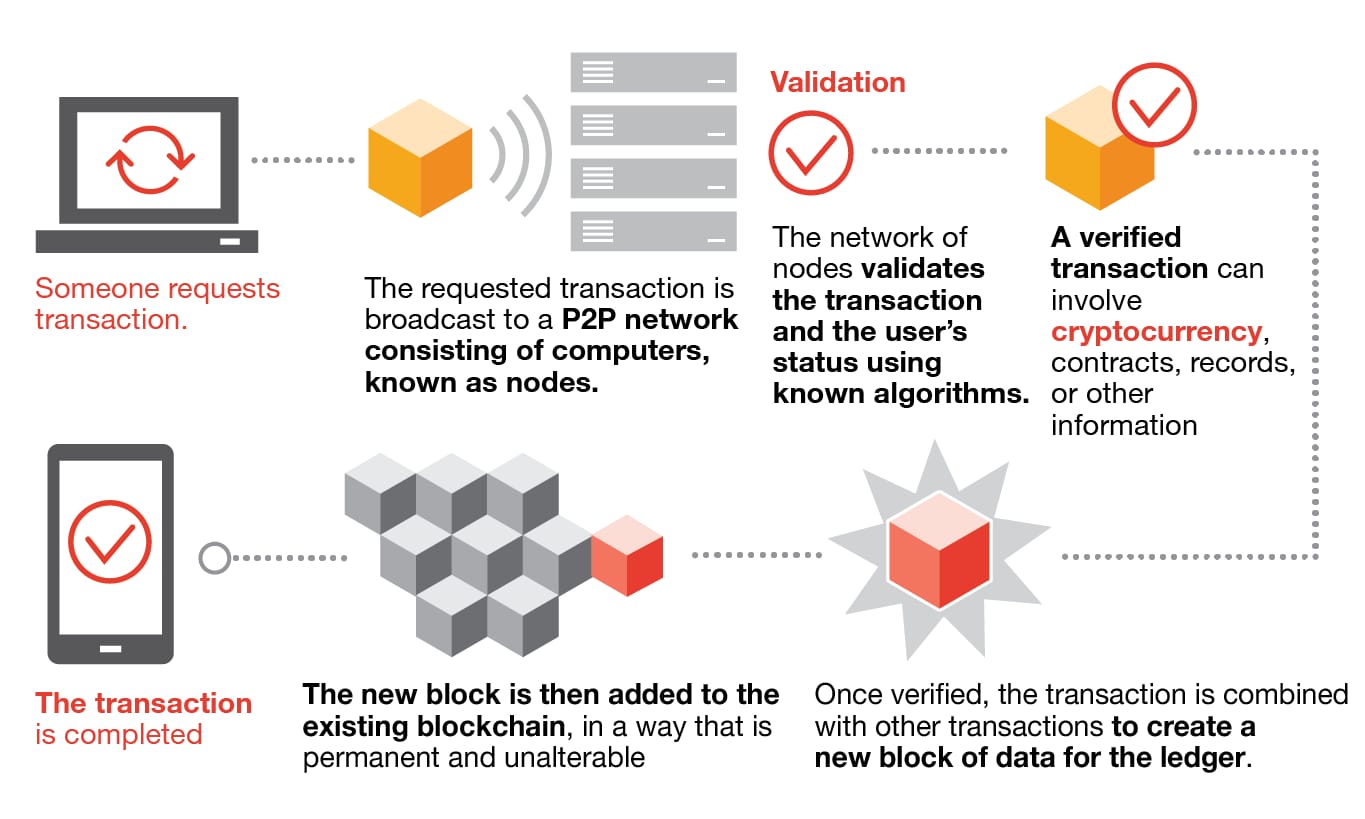

- Blockchain is a type of shared database that differs from a typical database in the way that it stores information; blockchains store data in blocks that are then linked together via cryptography.

- Simply put, a blockchain is a shared database or ledger. Pieces of data are stored in data structures known as blocks, and each node of the network has a replica of the entire database. Security is ensured since if somebody tries to edit or delete an entry in one copy of the ledger, the majority will not reflect this change and it will be rejected.

- As new data comes in, it is entered into a fresh block. Once the block is filled with data, it is chained onto the previous block, which makes the data chained together in chronological order.

- Different types of information can be stored on a blockchain, but the most common use so far has been as a ledger for transactions.

- In Bitcoin’s case, blockchain is used in a decentralized way so that no single person or group has control—rather, all users collectively retain control.

- Decentralized blockchains are immutable, which means that the data entered is irreversible. For Bitcoin, this means that transactions are permanently recorded and viewable to anyone.

2. What change can one expect from Blockchain

- Blockchain is a reliable way of storing data about other types of transactions as well. Some companies that have already incorporated blockchain include Walmart, Pfizer, AIG, Siemens, Unilever, and a host of others.

- By integrating blockchain into banks, consumers can see their transactions processed in as little as 10 minutes—basically the time it takes to add a block to the blockchain, regardless of holidays or the time of day or week.

- With blockchain, banks also have the opportunity to exchange funds between institutions more quickly and securely.

- By spreading its operations across a network of computers, blockchain allows transactions without the need for a central authority. This not only reduces risk but also eliminates many of the processing and transaction fees. It can also give those in countries with unstable currencies or financial infrastructures a more stable currency with more applications and a wider network of individuals and institutions with whom they can do business, both domestically and internationally.

- In India the process of recording property rights is both burdensome and inefficient; the process is not just costly and time-consuming—it is also prone to human error, where each inaccuracy makes tracking property ownership less efficient. Blockchain has the potential to eliminate physical functioning. If property ownership is stored and verified on the blockchain, owners can trust that their deed is accurate and permanently recorded.

- Blockchain aids smart contracts which can facilitate, verify, or negotiate a contract agreement.

- Blockchains can play a vital role in Supply chains as reported by Forbes, the food industry is increasingly adopting the use of blockchain to track the path and safety of food throughout the farm-to-user journey.

- Role of Blockchain in Elections- As mentioned above, blockchain could be used to facilitate a modern voting system. Voting with blockchain carries the potential to eliminate election fraud and boost voter turnout, as was tested in the November 2018 midterm elections in West Virginia.5 Using blockchain in this way would make votes nearly impossible to tamper with. The blockchain protocol would also maintain transparency in the electoral process, reducing the personnel needed to conduct an election and providing officials with nearly instant results. This would eliminate the need for recounts or any real concern that fraud might threaten the election.

3. The Advantages of Blockchain Technology

- Improved accuracy by removing human involvement in verification

- Cost reductions by eliminating third-party verification

- Decentralization makes it harder to tamper with

- Transactions are secure, private, and efficient

- Transparent technology

- Provides a banking alternative and a way to secure personal information for citizens of countries with unstable or underdeveloped governments

4. The disadvantages associated with Blockchain Technology

- Significant technology cost associated with data decentralisation.

- Low transactions per second

- History of use in illicit activities, such as on the dark web, money laundering and terror financing.

- Regulation varies by jurisdiction and remains uncertain

- Data storage limitations

- Lack of common consensus among major countries concerning the utilization of blockchain technology.

5. How can blockchain contribute to the Indian Economy

-

Accuracy of Blockchain Technology- Transactions on the blockchain network are approved by a network of thousands of computers. This removes almost all human involvement in the verification process, resulting in less human error and an accurate record of information.

-

Cost Reductions- Typically, consumers pay a bank to verify a transaction, and a notary to sign a document. Blockchain eliminates the need for third-party verification—and, with it, their associated costs.

-

Decentralization- Blockchain does not store any of its information in a central location. Instead, the blockchain is copied and spread across a network of computers.

-

Efficient Transactions- Transactions can be completed in as little as 10 minutes and can be considered secure after just a few hours. This is particularly useful for cross-border trades, which usually take much longer because of time zone issues and the fact that all parties must confirm payment processing.

-

Secure Transactions- Once a transaction is recorded, its authenticity must be verified by the blockchain network. Thousands of computers on the blockchain rush to confirm that the details of the purchase are correct. This discrepancy makes it extremely difficult for information on the blockchain to be changed without notice.

-

Transparency- Most blockchains are entirely open-source software. This means that anyone and everyone can view its code. This gives auditors the ability to review cryptocurrencies like Bitcoin for security.

-

Banking the Unbanked- Perhaps the most profound facet of blockchain is the ability for anyone, regardless of ethnicity, gender, or cultural background, to use it. According to The World Bank, an estimated 1.7 billion adults do not have bank accounts or any means of storing their money or wealth.7 Nearly all of these individuals live in developing countries, where the economy is in its infancy and entirely dependent on cash. Blockchains of the future are also looking for solutions to not only be a unit of account for wealth storage but also to store medical records, property rights, and a variety of other legal contracts.

6. Limitations in Pubic Digital Infrastructure

- Low availability and affordability: It is well established that digital infrastructure should be designed based on principles of availability, affordability, value, and trust.

- Current digital ecosystem is not interconnected as a design; a technical integration is required to make them conversant and interoperable.

- Validation of data is becoming complex: Information has to travel across multiple systems to complete the interaction and rely on private databases, which makes the validation of data more complex as the network grows, driving up costs and creating inefficiencies

6.1.How WEB 3.0 helps in overcoming public digital infrastructure

- WEB-3.0 is the next iteration of the internet. It heavily relies on blockchain technology, machine learning, and artificial intelligence (AI). It aims to create a decentralized internet with open, connected, intelligent websites and web applications.

7. Case studies- Countries across the world reap the benefits of BlockChain technology

- Estonia is the blockchain capital of the world and uses blockchain infrastructure to verify and process all e-governance services offered to the public.

- China launched a program in 2020 called BSN (Blockchain-based Service Network) to deploy blockchain applications in the cloud at a streamlined rate.

- The Brazilian government recently launched the Brazilian Blockchain Network to bring participating institutions into governance.

8. Need of the Hour

- There is a need for digital infrastructures such as blockchain technology to be designed based on principles of availability, affordability, value, and trust.

- The invisible rules underlying technology can be made visible using design principles, legislative frameworks, governance frameworks, and public engagement.

- The existing different digital infrastructures are not interconnected as a design; a technical integration is required to make them conversant and interoperable.

- It is becoming increasingly essential for developing nations to iteratively build innovative solutions on top of existing digital infrastructure.

- We need resilient platforms, which may be based on the Web3.0 architecture of tomorrow, even when we know it may take some more time to get these platforms capable of scaling and solving the current challenges in a cost-efficient manner.

- The Indian digital community, including fintech, academia, think tanks, and institutions, should focus on supporting research in standards, interoperability, and efficient handling of current known issues with the distributed technologies, e.g., scalability and performance, consensus mechanisms, and auto-detection of vulnerabilities

- A digital infrastructure based on blockchain technology will transform the digital ecosystem in India and will enable the future of digital services, platforms, applications, content, and solutions